Amazon Stock Prediction: Can AMZN Hit $305 in the Next 12 Months?

/amazon%20holiday%20delivery%20boxes%20by%20Cineberg%20via%20iStock.jpg)

Amazon (AMZN) stock has lagged the broader market in 2025, with shares climbing 4.2% year-to-date compared to the S&P 500 Index’s ($SPX) 12.96% gain. The ongoing macroeconomic uncertainty and an expected pressure on its operating income due to the company’s heavy spending on artificial intelligence (AI) and other innovations have kept the stock’s momentum in check.

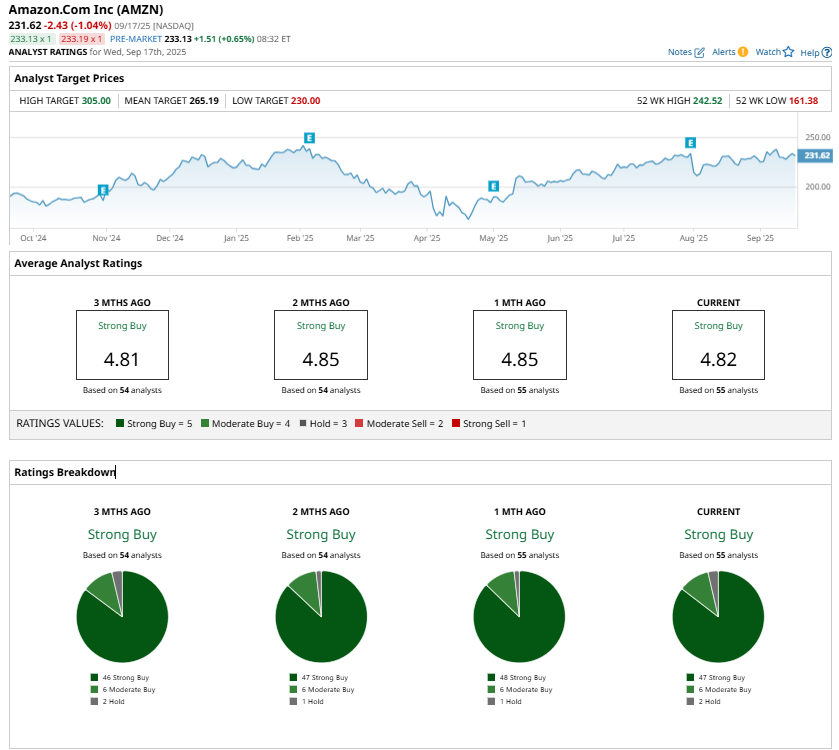

While AMZN stock has underperformed the broader market so far this year, will it rise about 32% from current levels over the next 12 months to hit the Street’s highest price target of $305? Let’s take a look.

Retail Resilience and Expanding Customer Reach

Amazon stock has been relatively quiet in 2025 so far, but its underlying business remains strong, suggesting significant upside potential. Notably, Wall Street’s sentiment toward the company is also positive. Amazon’s dominant position in e-commerce and cloud services augurs well for growth. Moreover, AI, automation, and advertising provide significant growth catalysts.

The company’s retail operations continue to thrive. Both online and physical stores are seeing healthy demand, supported by a combination of wide product selection, low prices, and fast shipping. Its recent moves to expand product offerings, including the return of Nike (NKE) merchandise and the addition of more premium brands, reflect its ability to attract both mainstream and upscale shoppers.

Another promising initiative has been the rollout of its perishables pilot, which lets customers add fresh items to their orders for same-day delivery from its fulfillment centers. The adoption of the service has been impressive, with three out of four customers trying the service this year being first-time buyers, and about 20% returned multiple times within the first month.

Third-party sellers remain another growth catalyst. Amazon continues to benefit from its marketplace model, where sellers add to product variety while helping drive competitive pricing.

Efficiency Gains Driving AMZN’s Profit Margins

Besides improving sales, Amazon is focused on improving profitability. For instance, in North America, operating income improved by $2.5 billion year-over-year in Q2, with margins expanding to 7.5%. The international segment also showed progress, with income rising to $1.5 billion and margins strengthening to 4.1%. These gains reflect productivity improvements across Amazon’s logistics network. Better inventory placement and stronger volume leverage have sped up delivery while keeping costs in check. Outbound shipping costs rose 6% year-over-year, but that was well below the 12% increase in unit growth, highlighting the efficiency improvements taking hold.

Looking ahead, Amazon is doubling down on robotics, automation, and strategic inventory placement to improve efficiency further. These investments will help reduce costs and enhance the customer experience through faster delivery.

Advertising: A Solid Growth Catalyst for AMZN

Another growth driver is advertising. Amazon Ads generated $15.7 billion in revenue last quarter, up 22% from the prior year. With access to an ad-supported audience of more than 300 million in the U.S. alone, the company is well-positioned to capture greater advertising spend. Its Demand Side Platform (DSP) allows advertisers to target audiences with precision. Recent partnerships have strengthened this offering, including a deal with Roku (ROKU) that brings Amazon’s DSP to 80 million connected TV households and an integration with Disney’s (DIS) ad exchange that grants access to premium streaming inventory. These moves further cement Amazon’s role as a major player in digital advertising.

AWS: The Cloud Giant and AI Catalyst

Meanwhile, Amazon Web Services (AWS) continues to deliver growth, with revenue climbing to $30.9 billion in the second quarter, up 17.5% year-over-year. AWS now has an annualized run rate above $123 billion, reflecting its dominant position in the cloud. Generative AI has become a key growth driver, driven by the ongoing shift of workloads to the cloud and the adoption of AI-driven applications. While AWS’s operating margins have dipped from record highs due to higher depreciation tied to heavy capital investments, these investments are expected to deliver long-term benefits.

Conclusion: Can Amazon Reach $305?

Amazon stock may be lagging the broader market this year, but its underlying business fundamentals remain strong. Retail is resilient, logistics are becoming more efficient, advertising is scaling rapidly, and AWS continues to dominate the cloud space while benefiting from the AI wave.

The short-term headwinds of macroeconomic uncertainty and rising capital expenditures are real, but Amazon’s long-term growth trajectory is solid. The company’s businesses are performing well, indicating that a rally toward the $305 price target over the next year is possible.

Analysts continue to rate AMZN as a “Strong Buy.”

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.